What This Article Covers

Community banks have historically struggled to offer profitable small-dollar loans due to high origination costs and legacy systems. Modern modular lending technology platforms now reduce origination costs by up to 80%, enabling banks and credit unions to digitize the full lending lifecycle and embed loans at the point of need — without core replacement.

The Transformation in Lending Tech in 2026

There was a time when GPS technology was reserved for aerospace programs and military operations. It powered satellites, guided aircraft, and supported billion-dollar missions.

Today, it helps a driver avoid traffic on the way home.

It powers your phone, your watch, and the app that tells you when dinner will arrive.

The technology itself didn’t change.

What changed was how it was delivered, and who could use it.

GPS became embedded, accessible, and scaled for everyday use. That shift didn’t make it any less powerful. It made it practical.

The same transformation is now happening in lending.

Why Small-Dollar Lending Hasn’t Worked for Community Banks

For years, modern digital lending infrastructure was built with only the largest banks in mind. The systems were powerful but complex. Capable but expensive. Effective, yet out of reach for most community banks and credit unions.

As customer expectations evolved, many smaller institutions found themselves caught in the middle. They wanted to offer fast, digital access to credit. They wanted to meet customers where needs actually arise. But the economics didn’t line up.

This wasn’t a lack of intent. It was a delivery problem.

Traditional lending stacks assumed large IT teams, multi-year transformation plans, and budgets that simply didn’t exist outside tier-1 banks. As a result, community banks were often forced to keep lending products confined to branches and manual workflows, even as fintechs and national players moved credit into apps, checkout flows, and point-of-sale experiences.

That gap is now closing.

The True Cost of Manual Loan Origination

Small-dollar and mid-ticket loans sit at the heart of many everyday financial needs. A car repair. A medical bill. A home improvement project. These are moments where customers look first to their bank.

Yet for many institutions, the numbers haven’t worked.

Manual processes and legacy systems can push origination costs to around $250 per loan. At that level, offering loans in the $500 to $3,000 range becomes economically unviable. The unit economics break down, even when the customer relationship is strong and the credit risk is manageable.

When community banks say no, customers don’t stop borrowing. They simply go elsewhere.

Fintech lenders and embedded financing providers step in with instant approvals and seamless digital experiences. Over time, community banks don’t just lose loan volume. They risk losing relevance.

Not because they care less about their customers, but because speed and accessibility increasingly define trust in lending.

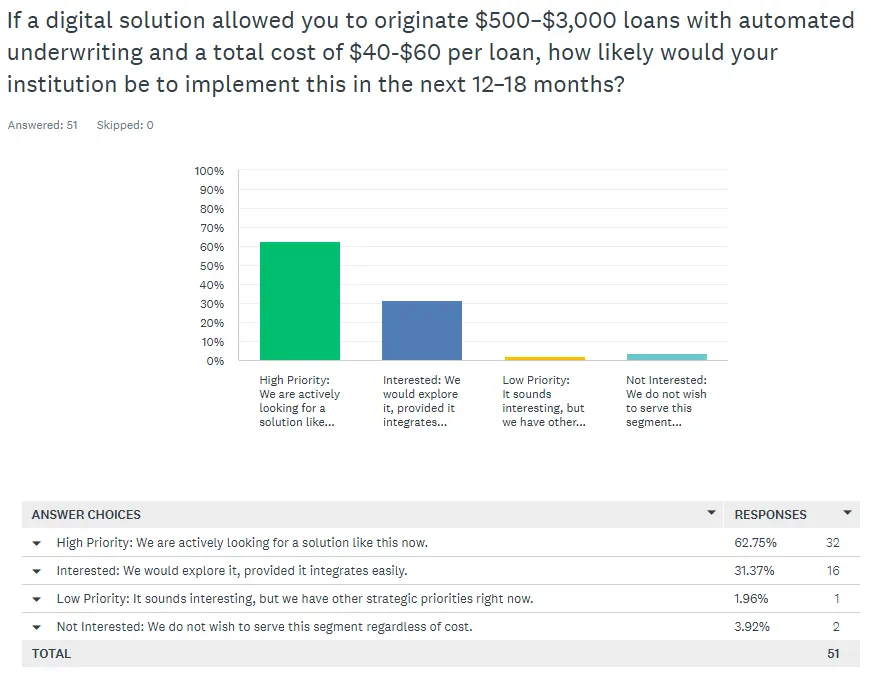

This reality is coming into sharper focus as banks plan for 2026. In a recent survey, 94% of community banks said they would be likely to adopt digital lending in the next year if the economics made sense.

The demand is there. The intent is there. The barrier has been delivery.

How Digital Lending Reduces Origination Costs by Up to 80%

Digitizing the full lending lifecycle changes the equation.

When origination, decisioning, disbursement, and servicing are automated end to end, origination costs can drop by as much as 80%. Suddenly, small-dollar loans are not just feasible. They’re sustainable.

The impact goes beyond cost savings.

Loans that once required branch visits can be delivered instantly through digital channels. Financing that was previously unavailable can be embedded directly into local businesses at the point of sale. Customers who might have turned to a fintech can be served by their own bank, on their own device, in the moment they need credit.

Even larger loans benefit. When the same infrastructure supports consumer and small business use cases, banks can extend financing into new contexts without adding operational complexity.

When the economics shift, lending stops being a constraint and starts becoming a growth lever.

Reinventing the Delivery, Not the Infrastructure

The GPS analogy is a useful reminder. Progress doesn’t always come from building something new. Often, it comes from making proven technology accessible to more people.

Community banks don’t need to rip and replace their core systems.

They don’t need a big-bank budget or a massive IT team.

They don’t need a multi-year transformation roadmap.

What they need are the same digital capabilities, delivered differently.

Modular Lending Platforms: Tier-1 Technology Without Tier-1 Complexity

Off-the-shelf, modular lending platforms now make it possible to “plug and lend.” The underlying technology is enterprise-grade. The difference is how it’s packaged, deployed, and scaled to fit the operating reality of smaller institutions.

Just as GPS became useful once it was embedded into everyday tools, digital lending becomes impactful when it fits naturally into a bank’s channels, workflows, and customer journeys.

When size stops dictating what’s possible, access becomes the advantage.

Progress isn’t always about inventing something new. Sometimes, it’s about making what already works available to everyone.

Manual processes and legacy systems can push origination costs to $200–$300 per loan, making $500–$3,000 installment loans economically difficult to offer.

By automating underwriting, KYC, decisioning, documentation, disbursement, and servicing, digital lending platforms significantly reduce operational overhead and manual intervention.

Embedded lending allows banks to offer financing directly within third-party environments such as merchant checkouts, ecommerce platforms, in-store systems, and partner ecosystems.

No. Modern modular lending platforms can integrate with existing core systems, eliminating the need for costly rip-and-replace initiatives.